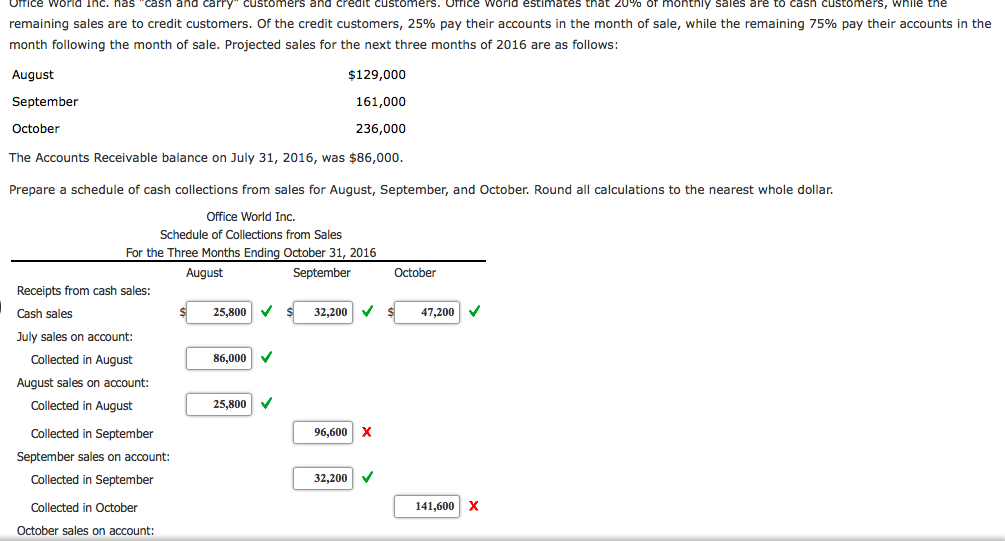

-

When low- otherwise zero-off costs is a good idea

When low- otherwise zero-off costs is a good idea We already oriented one to financial insurance rates (MI) often is despised from the those who have to invest it. Its expensive and its particular only work with goes to the financial institution instead than the resident.

But, if you do not rating a Virtual assistant or USDA mortgage, its near to unavoidable just in case you are unable to build a lower payment of at least 20% of one’s cost. Checked-out one other way, to quit expenses MI, your primary mortgage must be (features a great “loan-to-well worth proportion” (LTV) of) 80% or less of the purchase price. For most first-time consumers, that’s a close-impossible fantasy.

Just how piggyback funds performs

That have a piggyback mortgage, most of your mortgage talks about only 80% of your own purchase price. Very no MI is due thereon, however you make up the real difference having an additional mortgage and you can (usually) a deposit.

Piggy-back home loan combos get their names on the portion of the fresh new buy prices which you funds towards the second home loan. When you put 5% off, the loan are an enthusiastic 80-15-5. Your first home loan is 80%, the second is fifteen%, along with your downpayment was 5%. There are also 80-10-ten financing along with you putting 10% down.

Types of piggyback loans

Most people at present want its main home loan getting a 30-seasons, fixed-speed one, however you can select various varying speed mortgages (ARMs) with lower prices which might be fixed for as much as ten years.

Your “purchase-money second” home loan may be a fixed-rate financing, and safeguarded by the family. That implies you could deal with foreclosures or even pay it back due to the fact assented.

Have a much to expend your loan out-of from inside the ten, fifteen or 20 years. The less title can help you acquire family equity shorter and you will shell out shorter attract across the longevity of the borrowed funds. Although it does help the payment per month.

Dangers of piggyback loans

You should be able to find a great piggyback loan that suits your needs. However you need to come across your own personal carefully. In particular, be cautious about:

- Very early cancellation costs — aka brand new prepayment punishment. You don’t want to getting struck because of the large fees for individuals who later need to offer our home or refinance the home loan

- Balloon money — with your, your payment per month lies in a lesser amount of than the entire equilibrium. Thus, some or all the principal balance simply will get due within avoid of the name. Your own monthly installments can be mostly otherwise simply appeal, at the end, you may also are obligated to pay extreme lump sum.

By all means, talk to positives. However,, fundamentally, this is your occupations to make sure you understand what you may be committing so you’re able to. And that you is equipped to deal with one effects.

Assume you live in an area where home values is rising quickly. You might locate fairly easily that those rate increases are outstripping your capability to save yourself to possess an excellent 20% deposit otherwise only 5 percent. This could getting that buying mortgage insurance otherwise bringing a piggyback loan tends to make sound monetary experience.

You could undoubtedly work out if or not this applies to you; it is first mathematics. Play with HSH’s financial calculator to see what you are going to shell out to suit your mortgage if you buy now no downpayment or a low advance payment that. Also, tune home values on the areato see how far might possibly be shedding from the not being a resident. Sometimes, your choice might be a no-brainer.

And, while eligible for an effective Virtual assistant loan, that https://cashadvanceamerica.net/loans/loans-for-600-credit-score/ options is less difficult. With no continued home loan insurance premiums, you might be prone to select you are best off buying in lieu of leasing.