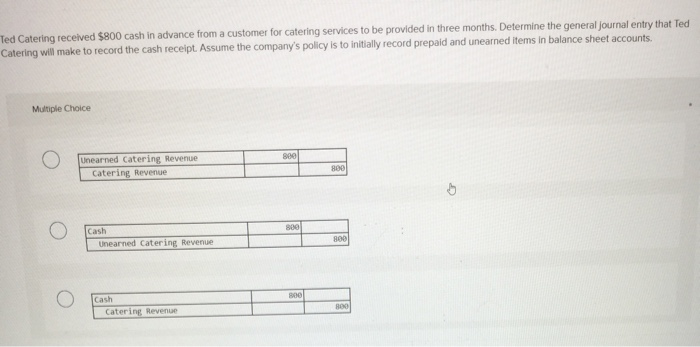

-

When it comes to nonconforming conventional loans, lenders is actually liberated to set their particular restrictions

When it comes to nonconforming conventional loans, lenders is actually liberated to set their particular restrictions Now that you’re always the brand new hallmarks out of a normal mortgage, you might be trying to find second strategies

Old-fashioned mortgage deposit standards The minimum deposit needed for a conventional home loan was step three%. It’s possible one to borrowers which have straight down credit scores or more loans-to-income percentages may be required so you can present increased down payment. Additionally, you will probably you want a bigger down payment to own an excellent jumbo loan otherwise that loan to own an extra household otherwise money spent.

Antique financing limitations The absolute most you can borrow having an effective old-fashioned mortgage depends on the type of old-fashioned mortgage Rio Vista cash advance you choose – compliant otherwise nonconforming.

Mortgage limits to own conforming antique fund are set by the Federal Property Money Company (FHFA), which provides supervision, control, and construction purpose supervision regarding Federal national mortgage association, Freddie Mac computer, together with Government Home loan Financial institutions. The current restriction was $647,two hundred in most U.S. areas, $970,800 from inside the areas which have higher can cost you out of living.

While there isn’t a traditional financing limitation per se, antique mortgage loans have to adhere to your neighborhood FHFA limitation becoming thought conforming.

Preapproval Before you start the program techniques, its demanded to reach out to a lender to have preapproval. They’re going to have to collect certain factual statements about your revenue, costs, and you will if or not you lease or own, to check the fitness because a borrower. With the an associated mention, they’re going to comment your credit score and credit file.

If it’s determined that you meet the preapproval criteria, the lending company offers a page stating that you’ve been preapproved for a particular amount borrowed. This can be a strategic circulate since having a letter out-of preapproval shows manufacturers that you are dedicated to to buy.

Authoritative Application for the loan Most lenders play with a basic application for the loan mode known as uniform residential application for the loan. Expect you’ll answer detailed questions regarding the type of mortgage, the house becoming ordered, as well as your personal earnings. Discover parts for your a position records, income, property, and you may debts.

And the software, you’ll want to furnish evidence of earnings eg pay stubs or tax statements over the past a couple of years. As the application is acquired, the lender requests a title writeup on the home and organizes getting an appraisal. Brand new label statement will find out if there are no a good liens against the assets, particularly a taxation lien. The fresh new appraisal find new fair market price of the house.

Underwriting From this point, underwriting find in case your loan application is eligible or refused. Loan providers have confidence in software programs to evaluate all the details towards the loan application to choose the exposure because the a borrower.

Closing While you are accepted to your financing after the underwriting procedure, the borrowed funds is considered “obvious to shut.” But not, in case the software is rejected, the lending company should provide you with a written factor.

In order to tie-up any loose ends up, you’ll meet with a closing broker in order to signal the mortgage data files. Mortgage loans wanted lots of records. After things are closed, the newest file bundle is distributed to share-closing to evaluate when it comes to mistakes. The borrowed funds usually money within a few days following closing usually.

The crucial thing to consider regarding the making an application for a mortgage is you don’t need to wade they alone. Whether it’s old-fashioned or any other tool, we are able to help you find the proper types of mortgage in order to make it easier to see your house to find fantasies. We are going to make it easier to compare, know about the new subtleties of each and every investment alternative to make an experienced choice according to your money and requirements. Even if you are unable to purchase property for the short term, we shall help you understand this making plans making your aim a reality.

Its fundamentally more straightforward to qualify for a normal mortgage that drops beneath the conforming financing restriction to suit your city

Conventional home loan loans-to-earnings conditions Brand new gold standard are a loans-to-money proportion (DTI) which is lower than thirty-six% getting conventional loans, even if sometimes a lender will get undertake a top DTI. To possess framework, their DTI signifies the total amount of your month-to-month debts (eg lease otherwise a car percentage) split by your pre-taxation month-to-month income.