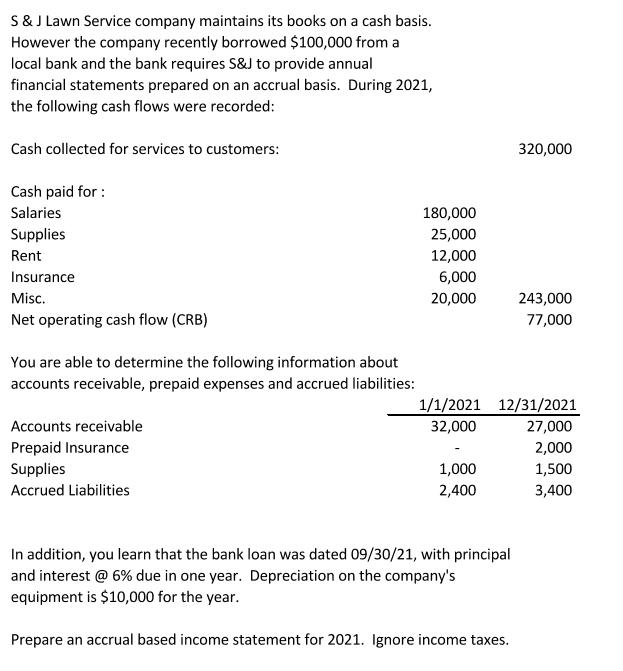

-

These types of records likely should include your tax returns, spend stubs, W-2s, W-9s, provide emails, and bank statements

These types of records likely should include your tax returns, spend stubs, W-2s, W-9s, provide emails, and bank statements What is actually underwriting?

Your own lending company spends underwriting when planning on taking steps to confirm your earnings, possessions, obligations, and you may assets details across the road to giving your residence loan. Its a way to reduce the mortgage lender’s exposure within the taking you towards the finance if you’re ensuring you can actually spend the money for domestic you want to purchase.

What do you prefer to own underwriting?

Your own home loan officer otherwise financial tend to require a selection of files you to answer questions regarding the income and capacity to manage the house.

The lender usually determine one loans you’ve got, such funds due into the vehicles, student education loans, credit cards, otherwise seats. The lending company looks at people advancing years discounts and you can investment. Drawn to one another, this type of paint an image of your financial wellness.

What goes on while in the underwriting?

An underwriter was a financial professional especially taught to do this style of risk comparison works. The person talks about your finances to determine just how much risk the lending company takes whenever they choose you be eligible for a good financing.

Essentially, so it underwriter determines in the event your mortgage would be accepted or otherwise not. They wish to make sure you never discovered home financing which you do not want and you may threats the lending company starting foreclosure legal proceeding.

#1: Comment your credit score

The credit report reveals your credit score and just how you made use of their borrowing in the past. It look for warning flags like bankruptcies, later costs, and you may overuse out-of borrowing from the bank. A very clear checklist with a good credit rating implies that your is actually in control on repaying expenses. That it improves your odds of financing recognition including ideal financing terminology and you can interest rates.

#2: Remark your house loans in Stebbins assessment

The latest underwriter feedback the brand new appraisal into the intended house. The brand new assessment is to check if the quantity youre inquiring to possess within the financial support aligns towards the home’s genuine worthy of. The new appraiser draws equivalent sales in the people and you can inspects the newest where you can find ensure that the price is practical.

#3: Verify your revenue

The newest underwriter needs to prove your own a job situation and genuine earnings. Your usually you desire three form of documents to confirm your income, including:

- W-2s on the last 24 months

- Current bank statements

- Your own latest pay stubs.

If you find yourself worry about-functioning or own an enormous share out-of a corporate, their underwriter will for several records such as your cash and you will losses sheet sets, equilibrium sheets, and private and team taxation statements.

#4: Determine the debt-to-earnings ratio

The debt-to-income proportion are a statistic that presents what kind of cash your purchase instead of how much money you earn. DTI is actually computed by adding your monthly minimal debt costs and you may separating it by your month-to-month pretax earnings. The latest underwriter measures up your debts on the earnings to confirm you have sufficient money to afford your monthly mortgage repayments, taxation, insurance policies.

And monthly income verification, lenders like to see the possessions because these shall be offered for the money for individuals who standard on your mortgage payments.

#5: Be certain that downpayment

Loan providers need to make sure you have got sufficient financing to fund the fresh deposit and you can settlement costs towards domestic pick. Underwriters as well as look at your lender comments and deals account so you can make sure to have the funds your deals and get contract contours you’d generate on closure.

Just how long do mortgage underwriting grab?

Based on how active new underwriter is actually, the latest acceptance procedure takes 2-3 business days to work through the many steps. Other people holds in the approval procedure, for instance the appraiser, identity insurance rates, and any other external items in the method.

Let speed along the underwriting procedure by the definitely replying to one requests in the cluster. Respond to any questions easily and you can truly. End opening the fresh new personal lines of credit inside the process, given that that complicate their acceptance.

After underwriting is finished.

Given that underwriter is finished, they approve, approve that have standards, suspend, otherwise reject the loan app. This new acceptance will give you the newest all the-obvious to close into the house pick. For other devotion, comment why to check out as much as possible do something so you can change your odds of another approval.