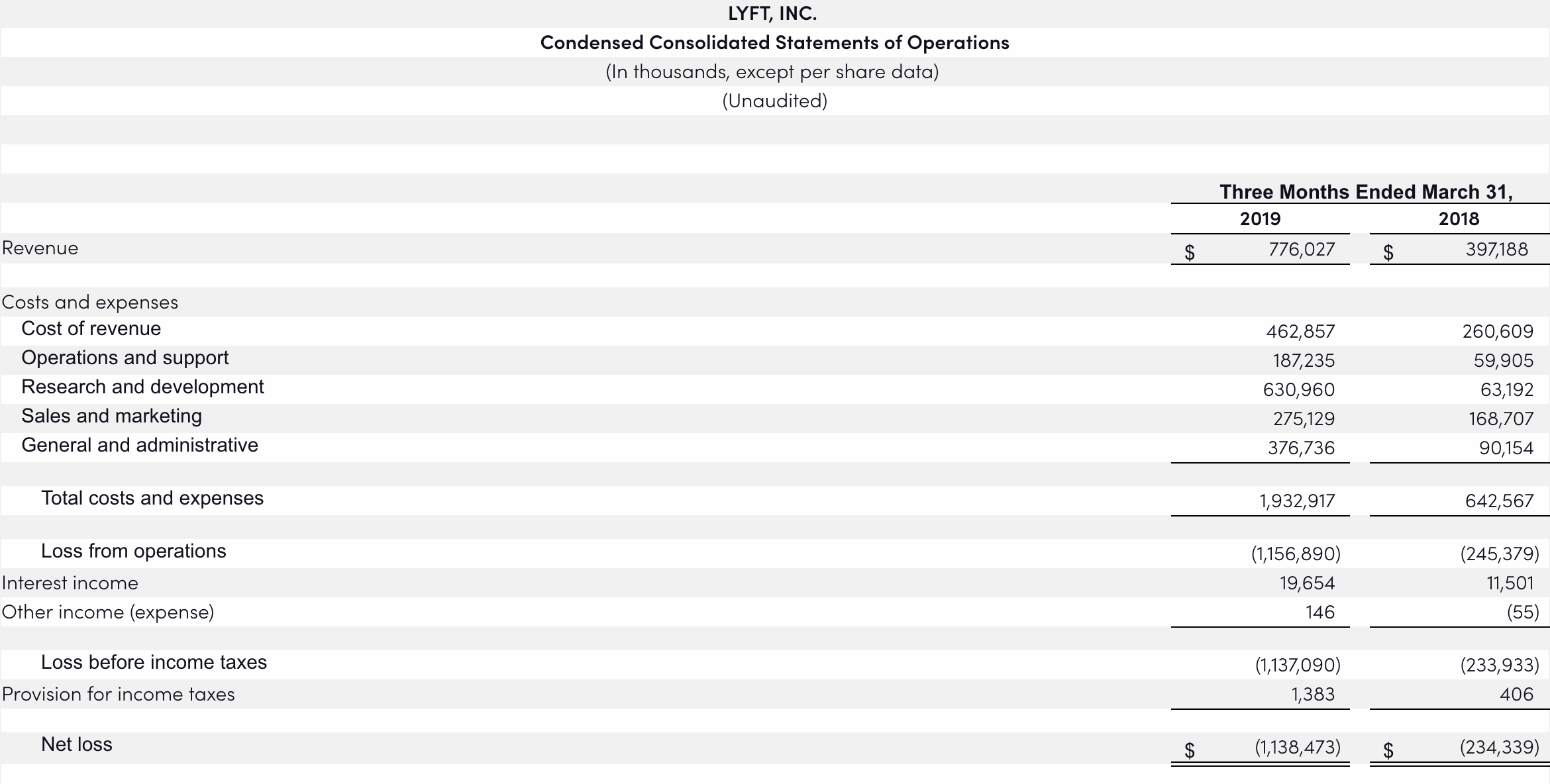

-

How PMI Is completely removed From the Payment per month

How PMI Is completely removed From the Payment per month Mortgage loans come in all of the sizes and shapes. Which is the best thing to possess potential housebuyers. It allows you to receive towards the home of your dreams using versatile terms and conditions. In many cases, personal home loan insurance can help help make your dream house you are able to.

What’s private home loan insurance rates? Consider individual mortgage insurance coverage, otherwise PMI, since the a defence arrange for the financial institution. It allows the fresh borrower to shop for a property that have less advance payment while protecting the lender meanwhile.

When you’re domestic browse as well as in industry to own an alternate home loan, studying anything you can also be towards techniques will help you create an educated decision from the and this mortgage to sign up for. Just the right mortgage could be as near as your credit partnership.

Just how Individual Home loan Insurance policies Work

/stop-payment-315346-Final2-78d2df2e17b84609806453f01e8f9fea.png)

Whenever lenders see a prospective borrower, they use one step-by-action verification strategy to dictate the right that the debtor commonly pay-off the whole mortgage. One of the strategies is the loan’s financing-to-really worth proportion, also known as the fresh LTV proportion.

That it LTV ratio is the amount borrowed asked toward really worth of purchased home. Loan providers play with 80 per cent just like the a tip. Financing are considered high risk in case your LTV proportion is higher than 80 percent.

Loan providers wanted a larger safety net to have safety, thus individual financial insurance policy is usually the earliest respond to. Personal mortgage insurance is paid in multiple implies:

Monthly

The most common technique for investing PMI premiums is by using your month-to-month loan fee. Your own month-to-month financing fee ought to include PITI-prominent, attract, taxation, and you will insurance rates. On top of that, their payment should include people financial insurance costs and you will homeowner’s organization charges, while the applicable.

Upfront Payments

Another option is always to pay the whole annual PMI payment upfront. Investing initial usually decrease your monthly homeloan payment, but you will have to be prepared for a far more significant yearly expenses before the PMI try reduced.

Hybrid

An alternative choice is a crossbreed of these two. You can spend a few of the PMI insurance premiums initial and use the remainder for the for each and every payment per month. This might help for those who have additional money to utilize and want your own monthly installments to stay reduced.

PMI is not a permanent part of your own payment per month. It is a protection coverage made to provide visibility if you do not arrive at the new 80 % LTV ratio. After you, this new borrower, pay down enough of their mortgage’s principal, as well as the LTV ratio falls lower than 80 %, you can cancel the brand new PMI.

When you’re buying PMI, once you have attained 20 percent collateral, you might get hold of your mortgage servicer and ask for to eradicate PMI from your own payment per month. By law, loan providers have to cancel PMI if the LTV ratio is placed so you’re able to visited 78 per cent. PMI usually immediately decrease conventional finance because the loan equilibrium reaches 78 per cent of the appraised well worth. Automatic PMI removing is called automated cancellation. Legally, the mortgage financial will minimize PMI withdrawal for free so you can you.

In case the house’s worthy of somewhat rises before you reach the newest 80 percent LTV, you might schedule another domestic appraisal to show your property may be worth more the initial amount borrowed. You’ll have to demand termination on paper in this case.

Is actually PMI An adverse Topic?

Of many homeowners view PMI once the just one more commission added into the with the loan amount. While that is true, PMI actually always an adverse topic.

Without personal financial insurance policies, you’ll most likely spend increased interest. As the loan providers just take a far more high exposure loaning money having a beneficial assets without much guarantee, which individual financial insurance rates discusses its exposure. Lenders are willing to leave you realistic costs because this assures them from percentage for many who standard with the mortgage.

By using PMI to get into a home, you can work to pay the balance down reduced, and that means you reach the 80 per cent endurance ultimately. Then you can cancel the PMI because you keep repaying the loan.

Just what PMI Will set you back

Pricing normally fall anywhere between 0.5 and you may step one.5 % of one’s total home mortgage count a-year. PMI will set you back may differ depending on multiple products, including:

LTV Ratio

The percentage change based on how far brand new house’s price is funded. A 3 per cent off mortgage will receive a higher PMI rate than simply you to in which the borrower places 10% down.

Credit score

Your credit score is among the trick indicators loan providers use to make the main points of your house loan, including the price of PMI. A good credit score commonly put you during the a reduced-exposure class, definition lenders offers a much better rate on the PMI.

Financing Sort of

Different varieties of funds hold various other levels of chance. For many who fund a fixed-price conventional financing, it’s smaller chance than just an adjustable-rates financial. And is shown in the matter you only pay getting PMI.

Manage Borrowing from the bank Unions Need PMI having Home loans?

Borrowing unions was user-run creditors offering similar services and products so you’re able to industrial banking institutions. He could be arranged furthermore and rehearse some of the exact same rules and you will rules, and requiring private home loan insurance rates having low LTV funds. However, credit unions are created to suffice their players. And as such, most of them bring many applications to greatly help participants get to their dreams of home ownership.

We understand many basic-day homeowners need assistance creating the desired down payment. That is why we’ve authored an initial-date homebuyer system , specifically for these types of participants. It allows that obtain up to 97 % of the home loan or price, any is gloomier. I provide seeds money mortgage assistance to loans your own closing and down-payment can cost you.

Require details? Inquire a specialist! While the an area borrowing connection, i endeavor to make it easier to navigate your money by using the most useful economic systems you can easily. How do we make it easier to?

On the New york Federal Borrowing Partnership North carolina Federal Borrowing Relationship is actually a good $900 mil-along with full-services, not-for-profit, collaborative standard installment loans Oakland NJ bank that has supported Vermonters for over 70 age, that have seven metropolitan areas currently providing more fifty,000 people. Players are included in a great collaborative, meaning it show possession in the Borrowing from the bank Relationship and you can elect a beneficial volunteer board from directors. North carolina Federal Borrowing from the bank Connection brings registration in order to anyone who lifetime, really works, worships, otherwise attends university inside New york. Vermont Government Borrowing Connection are committed to support its groups and you will providing Vermonters do well, regardless of where they’re with the life’s trip. Find out about Vermont Government Borrowing from the bank Union.