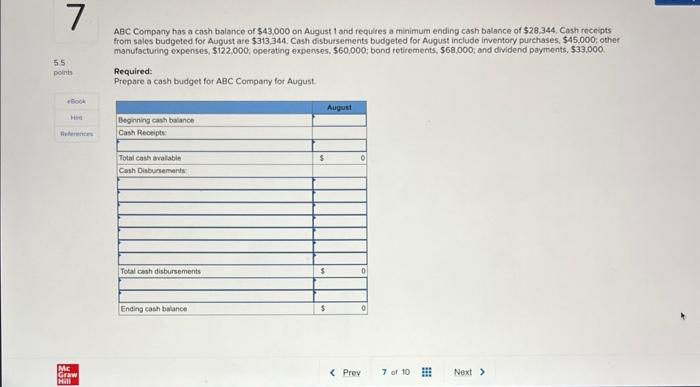

-

If they can confirm they could afford the loan and their money is actually constant, they are entitled to an equivalent loan therapy

If they can confirm they could afford the loan and their money is actually constant, they are entitled to an equivalent loan therapy To help you qualify, they will you prefer 90 days dominating, desire, real estate taxes, homeowner’s insurance coverage, and you can HOA fees in the a h2o membership like checking deals, Cds loan places Fairfield, or liquid opportunities.

If you’re a company, sales agent, otherwise associate, you have earned home financing just as much as individuals which have a beneficial salaried (W-2) reputation.

Brand new 1099 Money Program makes it a lot easier to help you secure a home loan even with working as good 1099 employee. No prepayment penalties into the manager-filled homes otherwise 2nd property as well as the allotment of up to 6% of one’s price for closing costs of curious people, i make it an easy task to safe resource to buy a home as the a beneficial 1099 worker.

- certification

I have built a powerful profile since the an excellent mortgage lender serving brand new lending means of realtors, builders, and you will private homeowners and you may homeowners. As the a full-solution mortgage lender, i’ve knowledgeable employees offering expertise in every area off home loan credit . out of purchase so you can re-finance so you can design lending. We offer usage of a complete list of mortgage offer and you will all our financing gurus are dedicated to finding the optimum mortgage – toward better rates, words, and costs – to get to know their own needs.

Evaluation

When deciding the appropriate being qualified earnings getting a home-operating debtor, it is vital to remember that providers earnings (especially regarding a collaboration otherwise S organization) stated on the a single Internal revenue service Function 1040 might not necessarily show money that in fact become shared with new debtor. The fundamental do so, whenever performing a home-a job earnings cash flow research, is always to determine the degree of money which might be relied into the by the debtor in the being qualified because of their personal financial responsibility. When underwriting this type of consumers, you will need to review business earnings distributions that happen to be generated otherwise could well be designed to such borrowers while keeping the brand new viability of your underlying team. So it investigation has determining the stability out-of providers income additionally the ability of company to carry on to create sufficient earnings so you can allow these types of individuals in order to satisfy the bills.

A few for a home-Working Borrower

the skill of the organization to keep creating and publishing enough earnings to enable the fresh new borrower to help make the repayments toward asked loan.

Duration of Self-Work

Federal national mortgage association fundamentally need lenders to acquire a two-year history of the latest borrower’s previous earnings as a means from indicating the likelihood that income will remain acquired.

But not, the amount of money out of a person who enjoys below a two-12 months reputation for care about-a position tends to be experienced, so long as brand new borrower’s most recent finalized individual and you may company government income tax productivity echo a complete season (one year) out-of self-a job income about current business. The borrowed funds file should incorporate records to help with the historical past out-of bill of early in the day earnings at the same (otherwise greater) top and you may

- in the an industry that provides a comparable goods and services since the the present day team, otherwise

- into the a profession in which they had similar duties to the people done regarding the the current organization.

In such instances, the lender need to bring careful consideration towards the character of borrower’s quantity of feel, and the quantity of obligations the organization provides acquired.

Verification of income

The financial institution get ensure a home-operating borrower’s a career and you can income because of the obtaining about borrower copies of the signed federal income tax returns (each other personal production and perhaps, team yields) that have been registered into Internal revenue service over the past 24 months (with applicable schedules connected).