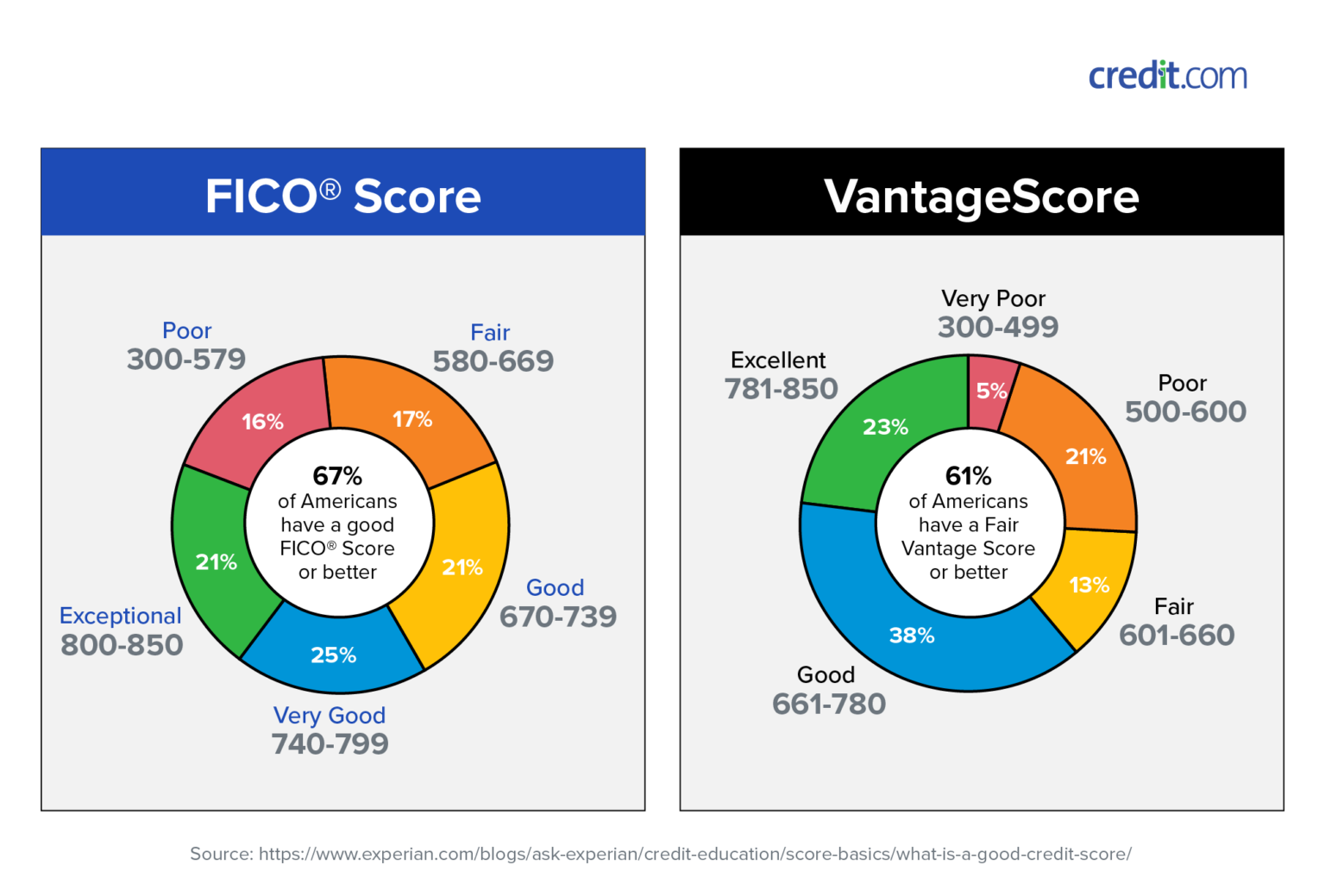

-

Simply how much home loan notice can you deduct on the taxes?

Simply how much home loan notice can you deduct on the taxes? The borrowed funds attention deduction used to be a mainstay to possess customers, nevertheless earlier long-time features changed one . Particular property owners could be best off perhaps not saying one to deduction.

In the event you need cash advance america in Orchard Colorado to allege they, discover less than to find out how it works – and in case it’s wise for your requirements.

How exactly to subtract home loan focus with the government tax statements

After you file taxation, you can use the practical deduction or the itemized deduction. Inside the 2022, the product quality deduction is $25,900 for maried people submitting as you and you can $a dozen,950 for people. The standard deduction is actually $19,eight hundred for those submitting as lead away from household.

The mortgage interest deduction is only accessible to people who itemize its write-offs. By taking the quality deduction, you might not be able to deduct your own home loan appeal. And because the high quality deduction is indeed high, most people are better out of perhaps not itemizing their deductions.

Generally speaking, you ought to merely itemize the write-offs if your total amount is higher than the quality deduction. Can help you the brand new math your self otherwise hire a keen accountant in the event the you prefer a great deal more direction.

You can subtract attract with the a house security mortgage otherwise line of credit, for as long as your house try listed given that security. In the event that another type of little bit of house is indexed because security, then you can be unable to deduct the attention.

Depending on the measurements of your own mortgage, subtracting financial notice tends to be one of the largest deductions your helps make and certainly will significantly decrease your taxable income.

Tax thinking software can easily make it easier to determine how far so you’re able to deduct. Get the taxation done properly as well as your maxim refund secured having TurboTax here.

Simple tips to deduct mortgage attention to your condition taxation statements

In case your county fees tax, you might be able to subtract their mortgage attention on your condition tax returns. However, exactly how much you can deduct and any other restrictions depends on your specific country’s legislation.

If you want to subtract the attention, you can utilize this new numbers on the 1098 form delivered because of the your mortgage lender. Or even receive a good 1098 function, which can mean that you reduced lower than $600 into the attract. not, you need to be able to subtract the mortgage attention. You’ll only have to by hand determine the degree of interest paid in overall.

Some claims possess a limit about precisely how of many qualities your can also be subtract the mortgage notice to possess, while some claims enables you to subtract the eye into the all of the your property.

How-to be eligible for the mortgage appeal deduction

Just property owners whoever financial financial obligation was $750,000 or shorter is subtract the home loan focus. When you find yourself married submitting independently, you could merely subtract financial notice in the event your home loan personal debt are $375,000 otherwise less.

The fresh restriction had previously been $1 million, but one changed following the passage through of the latest 2017 Taxation Incisions and Operate Act.

Subtracting financial appeal towards the next home

When you have a couple land , you can nonetheless deduct the loan interest in your government taxation on the another domestic. In order to qualify, the house should be noted as equity on mortgage. You could potentially simply subtract focus using one house besides the majority of your possessions.

But not, the rules vary in the event the second residence is a rental possessions. In this case, you could only take the new deduction if you’re on possessions for 14 days or 10% of time it is rented. For those who never are now living in it, then it is only handled because a rental property you can not take the mortgage focus deduction.